For millions of retirees, disabled workers, and surviving family members, Social Security is not optional income. It is the financial backbone that supports daily life. Monthly checks help cover groceries, prescription drugs, housing costs, utilities, insurance premiums, and transportation. That reality is why the annual Cost-of-Living Adjustment, known as COLA, remains one of the most closely watched updates in the U.S. financial system.

As attention turns toward 2026, early projections for the Social Security COLA are already shaping expectations. Inflation has cooled from the sharp spikes seen earlier in the decade, but everyday costs remain elevated, particularly in healthcare and housing. Current estimates suggest the 2026 COLA could fall between 2.6% and 3.0%, a range that may appear modest but carries meaningful consequences for households that depend on fixed incomes.

Why the COLA Matters in Today’s Economy

The COLA exists for one core reason: to prevent inflation from silently eroding the value of Social Security benefits. Even when price increases slow, they rarely reverse. Rent continues to rise, insurance premiums trend upward, and medical expenses often increase faster than the overall economy.

Without annual adjustments, beneficiaries would lose purchasing power year after year. The COLA is not designed to improve lifestyles or create surplus income. Its purpose is protection. It helps beneficiaries maintain roughly the same standard of living despite higher prices. In an environment where many seniors have limited savings and little opportunity to increase earnings, that protection is more critical than ever.

Early Projections for the 2026 COLA

Based on inflation data through late 2025, analysts are currently estimating a COLA increase in the 2.6% to 3.0% range for 2026. These projections are tied to consumer price trends in essential categories such as food, housing, transportation, and energy.

If the increase lands near the middle of that range, the average monthly retirement benefit could rise by approximately $50 to $65. For someone receiving $2,000 per month, that would translate to a new benefit of around $2,060. While the monthly change may seem small, over a full year it adds up to several hundred dollars, often enough to offset rising prescription costs or insurance premiums.

For households managing tight budgets, that additional income can reduce financial strain and improve stability, even if it does not fully eliminate cost pressures.

How the Social Security Administration Calculates COLA

The COLA is not influenced by political debate or discretionary decisions. The Social Security Administration uses a specific formula tied to the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). This index tracks price changes for commonly purchased goods and services, including groceries, transportation, housing, and energy.

Each year, the SSA compares CPI-W data from July, August, and September with the same three-month period from the previous year. If prices have increased, benefits are adjusted upward by the same percentage. If inflation is flat or negative, benefits remain unchanged.

This automatic system ensures consistency and predictability. However, it is not without criticism. Many experts argue that CPI-W does not fully reflect senior spending patterns, particularly the outsized role healthcare plays in older households. Medical expenses often rise faster than general inflation, which can leave some beneficiaries feeling that COLA increases lag behind real-world costs.

Who Is Eligible for the 2026 COLA Increase

Every individual receiving Social Security benefits is eligible for the COLA. This includes retired workers, disabled workers receiving SSDI, survivors, and Supplemental Security Income recipients. The adjustment applies automatically, and no application is required.

The percentage increase is the same for everyone, but the dollar impact varies. Beneficiaries with higher monthly payments receive larger dollar increases, while those with smaller benefits often feel the adjustment more immediately because nearly all of their income goes toward essentials.

Older retirees, especially those over age 75, tend to rely more heavily on Social Security as savings decline. For this group, the COLA often plays a crucial role in covering rising healthcare and long-term care costs.

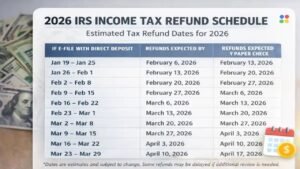

When the 2026 COLA Will Take Effect

The Social Security Administration is expected to announce the official 2026 COLA in October 2025. Beneficiaries typically receive mailed or online notices in December outlining their updated benefit amounts. The increased payments begin with checks issued in January 2026.

Because Social Security payments are distributed on a staggered schedule based on birth dates, not everyone sees the increase on the same day. However, all January payments will reflect the new COLA-adjusted amounts.

Broader Economic Impact of COLA Increases

While COLA is not a stimulus program, it does have ripple effects throughout the economy. When tens of millions of Americans receive slightly higher monthly payments, that money is quickly spent on necessities. Grocery stores, pharmacies, medical providers, landlords, and utility companies all feel the impact.

In communities with large retiree populations, COLA increases can help stabilize local economies by maintaining steady consumer spending. The adjustment offsets higher prices rather than creating new demand, but it still plays a role in economic balance at the local level.

Planning Realistically Around the COLA

Financial experts consistently advise viewing the COLA as an adjustment, not a raise. While it helps maintain purchasing power, it rarely covers all rising expenses, especially during periods when healthcare costs increase rapidly.

Beneficiaries are encouraged to combine Social Security income with careful budgeting, emergency savings when possible, and regular financial reviews. Even modest COLA increases can be more effective when paired with proactive planning and realistic expectations.

Looking Ahead

The projected 2026 COLA reflects an economy that is stabilizing but still expensive. A 2.6% to 3.0% increase would provide meaningful relief for many households, even if it does not fully offset rising costs. As always, the official figure will depend on inflation data through the third quarter of 2025.

For those who depend on Social Security, staying informed through official SSA updates remains the best way to prepare. The COLA may not solve every financial challenge, but it continues to serve as a critical safeguard for millions of Americans navigating retirement and disability in a high-cost world.

Disclaimer

This article is for general informational and educational purposes only and does not constitute financial, legal, tax, or retirement planning advice. Social Security rules, inflation measures, and COLA calculations may change based on federal policy and economic conditions. Individual benefit amounts vary. Readers should consult official Social Security Administration resources or a qualified financial professional for guidance specific to their situation.