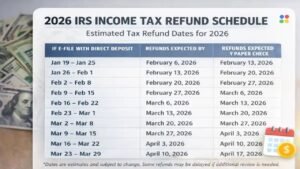

For decades, the U.S. tax refund served as a reliable financial checkpoint for millions of households. File your return, wait a few weeks, and a lump sum—often between $1,000 and $3,000—arrives in your bank account. In 2026, that rhythm is shifting. Taxpayers are noticing slower refunds, unexpected amounts, and a sense that predictability has eroded.

These changes are not caused by sudden tax law alterations or headline-grabbing legislation. Instead, they reflect structural evolution within the IRS, including enhanced data-matching systems, tighter fraud prevention, and individualized return reviews. For families who rely on refunds to pay bills, manage tuition, or bolster savings, these shifts carry tangible consequences.

How IRS Refund Processing Reached This Turning Point

The uncertainty surrounding refunds has roots in pandemic-era backlogs. Legacy IRS systems struggled under the weight of paper returns, overloaded call centers, and delayed filings. In response, the agency accelerated automation and real-time verification, embedding these improvements into everyday processing by 2026.

Unlike the past, returns are no longer processed in broad batches. Each return undergoes risk-based screening, cross-referenced against employer reports, bank data, and prior filing patterns. Two taxpayers with similar incomes may experience different timelines if one return triggers even minor discrepancies. Accuracy has improved, but predictability has decreased, especially for those accustomed to fast, routine refunds.

Why the $1,000–$3,000 Refund Benchmark Is Losing Relevance

The notion that a “normal” refund falls between $1,000 and $3,000 emerged in eras of stable employment and predictable withholding. Today, irregular income from gig work, bonuses, or variable hours has blurred the lines. Refund amounts now reflect these shifts, often appearing as financial surprises rather than errors.

Tax analyst Kavita Rao explains, “Refunds feel like surprises, but they are really delayed mirrors. What changed in your income shows up only when you file.” Many households are caught off guard, not because the IRS made a mistake, but because expectations no longer match modern earning patterns.

Credits, Verification, and the New Delay Dynamic

Refundable tax credits remain a key source of delay. Returns claiming credits such as the Earned Income Tax Credit (EITC) or Child Tax Credit are automatically routed through additional verification checks. These safeguards prevent improper payments but also slow refund timing for households that depend on them most.

Even small changes—new bank accounts, address updates, or income variations—can trigger extra confirmation steps. These reviews are algorithm-driven, not personal, and are often invisible to taxpayers. The result: a return may appear “stuck” online, even though it is simply moving through the IRS verification queue.

When Approval Doesn’t Mean Immediate Deposit

Another layer of complexity occurs after a refund is approved. Banks handle deposits differently: some release funds immediately, while others hold them for internal verification. Two taxpayers with identical IRS approval dates may see deposits days apart. Faster data processing at the IRS paradoxically can slow the final step if filings arrive before all employer forms or confirmations are completed.

Who Feels the Strain Most

Lower- and middle-income households are disproportionately affected. Many plan their monthly budget around refunds, relying on them to cover bills, tuition, or debt. Delays or reduced amounts can force households to turn to credit cards, payday loans, or deferred payments.

Wealthier taxpayers, with diversified financial buffers, are less reliant on refunds, highlighting a growing inequality in the impact of IRS processing changes. Administrative efficiency does not always translate into household convenience, and those with less flexibility often bear the brunt.

The Future of IRS Refund Processing

Experts anticipate these trends will continue. Automation will expand, and individualized processing will become standard. Fraud prevention will remain rigorous, with fewer blanket timelines and more targeted reviews. From an operational standpoint, this is progress.

For taxpayers, however, the shift is as much psychological as it is financial. Advisors now recommend treating refunds as unexpected bonuses rather than guaranteed income, and planning expenses accordingly. Flexibility, rather than assumption, is emerging as the most prudent approach.

Key Takeaways

- Refund timelines are increasingly influenced by verification steps, credit claims, and changes in personal financial data.

- The traditional $1,000–$3,000 refund expectation is less relevant for modern income patterns.

- Algorithm-driven checks, bank processing, and employer reporting affect when funds appear.

- Taxpayers should treat refunds as variable income and avoid budgeting critical expenses solely on their arrival.

2026 marks a turning point in IRS refund processing: faster, more accurate, and safer, but less predictable. Understanding these shifts and adjusting expectations is essential for households navigating the changing financial landscape.

Disclaimer: This article is for informational purposes only and does not constitute legal, financial, or tax advice. Refund amounts, IRS procedures, and individual circumstances vary. Consult qualified professionals or official IRS resources for guidance specific to your situation.