As January 2026 unfolds, a familiar figure is capturing national attention once again: $2,000. Reports suggest the IRS may issue a one-time direct deposit during the month, targeting households in need of short-term relief. With high grocery bills, rising rent, and winter utility costs, the possibility of federal support has sparked widespread interest and conversation.

Unlike pandemic-era stimulus checks that followed formal legislation and broad announcements, this payment is said to be quieter and more targeted, using existing IRS payment infrastructure rather than requiring new programs. Even if the details are still evolving, the story highlights the ongoing financial pressure faced by millions of Americans entering 2026.

Why the $2,000 Figure Has Resurfaced

The reappearance of this number is not coincidental. Inflation, although moderated on paper, has left everyday costs high for many families. Winter heating, rising insurance premiums, and stagnant wages combine to make even modest federal assistance meaningful.

Historical memory also plays a role. Americans became accustomed to direct deposits of relief funds in 2020–2021, with minimal paperwork and fast delivery. When news of a potential $2,000 deposit emerged, many assumed a similar approach: leverage existing tax data to deliver funds quickly, without launching a new welfare program.

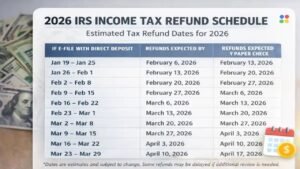

How This Payment Differs From a Tax Refund

Crucially, this reported deposit is not a tax refund. Refunds return overpaid taxes, while this payment is framed as relief assistance, independent of what a taxpayer owes. Timing is another distinction: while tax refunds typically follow filing season schedules into February or March, the $2,000 deposits are reported to begin in January, using 2024 or 2025 tax data to assess eligibility. This allows households to receive support during the peak of post-holiday financial strain.

Who Stands to Benefit

Current reports suggest low- and middle-income households will gain the most. Income thresholds resemble previous relief efforts: single filers earning up to $75,000 and married couples filing jointly up to $150,000 may qualify for the full payment, with phased reductions above these limits.

Families with dependents are likely central to the distribution. Past IRS-administered relief programs accounted for household size, meaning parents juggling childcare, education, and medical costs could see meaningful short-term support. As fictional tax policy analyst Daniel Morris notes, “Targeted cash support flows directly into local economies because families spend it immediately on essentials.”

Distribution Timing and Potential Delays

Reports indicate deposits will be released in waves throughout January 2026, beginning with taxpayers who have direct deposit information on file. This staggered approach mirrors previous stimulus rollouts and helps reduce system overload and errors.

Delays may still occur for those without updated banking information, potentially pushing paper check deliveries into later weeks. Financial counselors warn that recent address changes or mismatched account details are common sources of slower payments. Consequently, two households with similar incomes may experience very different timelines, even if the system functions correctly.

Public Reaction and Expert Insights

Public response has been mixed. Some celebrate early, sharing posts announcing incoming relief, while others caution against misinformation and potential scams. History has shown that rumors of payments often circulate before official confirmation, leaving some households disappointed or vulnerable.

Experts advise monitoring official IRS announcements closely. If formal statements clarify the program, confidence and planning will improve quickly. Otherwise, discussions may pivot to standard tax refunds. As Morris emphasizes, “Short-term payments don’t solve structural issues, but they buy time, and sometimes that’s exactly what households need.”

What This Reveals About Economic Pressures in 2026

Beyond the payment itself, the discussion underscores the persistent financial strain in American households. That a potential $2,000 deposit can dominate national conversation reflects ongoing fragility: many families are not seeking windfalls, but breathing room.

If confirmed, the payment will likely be remembered for its timing rather than policy design. January is traditionally a month of peak expenses and low savings, making even a modest infusion impactful. The narrative highlights how much short-term support can matter when economic stability feels temporary.

Key Takeaways

- The reported January 2026 $2,000 deposit is distinct from tax refunds and intended as short-term relief.

- Eligibility appears targeted toward low- and middle-income households, with sliding-scale reductions for higher earners.

- Timing and distribution may vary, with direct deposits prioritized and paper checks following later.

- Official IRS announcements should be monitored carefully to avoid scams or misinformation.

- The conversation reflects broader economic pressures and the importance of timely household support.

Disclaimer: This article is based on publicly circulating reports and discussions regarding a potential IRS-administered $2,000 direct deposit in January 2026. It is intended for informational purposes only and should not be treated as financial, legal, or tax advice. Readers should rely on official IRS announcements and verified government sources before taking action or sharing personal information.