As January 2026 approaches, many taxpayers are closely monitoring reports about a potential $2,000 IRS deposit. This payment is part of a targeted federal program and is not intended for every American. It is not a loan and does not need to be repaid.

The deposit is issued based on tax records already on file with the IRS and is designed to provide financial relief for eligible individuals. It is separate from monthly benefits or other routine federal payments, focusing on taxpayers who meet specific eligibility requirements.

Who May Qualify for the Payment

Eligibility for the $2,000 IRS deposit depends on several factors:

- Filing Status: Single, married, or head-of-household filing affects income limits.

- Adjusted Gross Income (AGI): Payments are limited to those below thresholds published by the IRS.

- Dependents: Eligible dependents claimed on a prior year’s tax return may increase the total amount.

- Residency & Identification: Must be a U.S. resident with a valid Social Security number.

Nonresident aliens and ITIN filers are generally excluded unless the IRS specifies otherwise. Individuals must have filed the required tax return for the previous year to be considered.

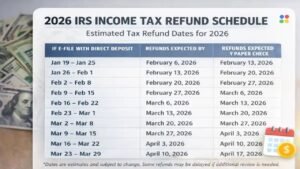

When and How the Payment Is Sent

The IRS plans to distribute the $2,000 deposit in waves throughout January 2026.

- Direct Deposit: Taxpayers with banking information on file will typically receive funds electronically. These deposits may appear as pending for a few business days before fully posting.

- Paper Checks or Debit Cards: For those without direct deposit information, the IRS will mail payments. Delivery may take longer due to postal processing.

What to Do If You Do Not Receive the Deposit

Not receiving the payment does not automatically mean you are ineligible. The IRS generally allows taxpayers to claim missing payments when filing their tax return for the relevant year.

Before taking any steps, it’s recommended to:

- Check official IRS online tools for payment status.

- Confirm your banking and personal information is current.

- Keep documentation of previous tax filings and IRS notices.

Handling Errors or Wrong Deposits

If the deposit goes to an incorrect or old bank account, contact both your bank and the IRS immediately. Avoid spending funds received by mistake, as returning incorrect payments promptly can prevent legal or administrative issues.

Maintaining clear records, including tax documents and bank statements, is advised for at least three years in case of discrepancies.

Why Keeping Information Updated Matters

Delays often occur due to outdated addresses or banking details. Taxpayers who have moved, closed accounts, or changed financial institutions should update their information promptly through:

- Their next tax return

- The IRS online account portal

Quick updates help ensure smooth processing and reduce the risk of missing or misdirected payments.

Final Thoughts

The IRS $2,000 deposit for January 2026 is genuine for eligible taxpayers, but it is not automatic for everyone. Understanding eligibility, monitoring official IRS tools, and keeping records up to date are crucial steps to ensure receipt of the payment if you qualify.

Disclaimer

This article is for informational purposes only and does not constitute tax, legal, or financial advice. IRS rules, eligibility criteria, and payment schedules may change. Readers should consult official IRS resources or a qualified tax professional for guidance specific to their circumstances.