As January 2026 begins, discussions of an IRS $2,000 direct deposit have resurfaced across households nationwide. The conversation is no longer confined to tax forums or financial blogs; it has permeated social media feeds, office chatter, and even family discussions. For households managing higher rent, post-holiday bills, and rising grocery costs, the prospect of early-year federal support carries both financial and emotional significance.

Yet, the reality behind these claims is far more nuanced. Unlike pandemic-era stimulus checks, which followed clear legislative approval, the current $2,000 narrative stems from partial information, prior policy experiences, and online amplification. The IRS has not formally announced a universal payment, and conflating expectations with confirmed policy can lead to costly financial missteps.

Why the $2,000 Figure Keeps Reappearing

The number $2,000 is not arbitrary. It echoes previous pandemic-era stimulus payments that served as lifelines for millions of Americans. That familiarity makes the figure psychologically persuasive, especially when discussions about tax credits, refunds, or proposed relief measures surface online.

Digital platforms accelerate the spread of partial information. Screenshots of proposals or misread IRS updates can go viral, creating a perception of certainty even when official guidance is absent. As public finance researcher Anil Deshmukh observes, “People don’t invent these numbers out of thin air. They come from memory, and memory can be persuasive even when outdated.”

What the IRS Has Clarified

Officially, the IRS has not confirmed a standalone $2,000 direct deposit program for January 2026. What has been confirmed is routine: changes in refund timelines and adjustments to existing tax credits that may result in larger refunds for some filers. In certain cases, these refunds can approach or exceed $2,000, particularly for households claiming multiple credits.

It is important to distinguish between a refund and a relief payment. Direct federal payments require explicit authorization from Congress and detailed IRS guidance. Until legislation is enacted, any specific payment amount should be treated as speculative.

Eligibility Talk and the Comfort of Familiar Thresholds

Much of the credibility surrounding $2,000 claims stems from familiar income thresholds—figures like $75,000 for individuals or $150,000 for couples—which mirror past relief programs. Familiar numbers feel trustworthy, reinforcing the perception that the payment is imminent.

However, similarity does not equal confirmation. Past relief programs included clear eligibility rules codified in law. Planning expenses around unverified payments is risky, particularly for families already operating under tight budgets. Financial experts caution that assumptions about incoming funds can exacerbate stress if the deposits fail to materialize.

Why January Timing Fuels Expectation

January is historically a pressure point for household finances. Heating bills peak, insurance premiums reset, and holiday debts come due. In this context, a rumored $2,000 IRS deposit seems perfectly timed.

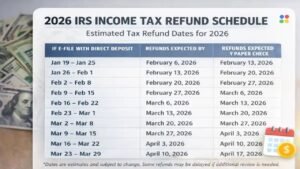

Yet even confirmed refunds can be delayed due to verification checks, processing backlogs, or variations in bank handling. History shows that announced dates often serve as estimates. Until funds are officially deposited, financial planning should remain conservative.

Public Reaction and Scam Risks

Responses to $2,000 payment rumors have been mixed. Some celebrate and share posts claiming deposits are “on the way,” while others voice skepticism. Both reactions reflect genuine concern, but the environment also attracts scammers, who impersonate IRS officials to extract personal information or fees.

The IRS consistently warns that it does not initiate contact through text messages or social media. Legitimate updates appear on official government websites or through established news outlets. Any payment program would be accompanied by formal documentation and public guidance.

Key Takeaways

- Monitor official sources: Only rely on IRS.gov or U.S. Treasury announcements.

- Understand refunds versus relief payments: Refunds are reconciliations of prior tax payments and credits; relief payments require congressional approval.

- Avoid sharing personal information: Be alert for phishing attempts using IRS branding or urgent language.

- Plan cautiously: Do not budget for unconfirmed funds; unexpected deposits may occur, but they are not universal payments.

Looking Ahead

Speculation thrives when financial anxiety intersects with fragmented information. While targeted relief programs or adjustments to tax credits are possible in the future, certainty requires legislation and formal IRS guidance. Until then, treating unconfirmed $2,000 deposit claims as informational noise is the safest approach. Filing taxes accurately, monitoring official updates, and maintaining conservative financial planning remain the most reliable strategies for households entering 2026.

Disclaimer: This article is for informational purposes only and does not constitute legal, tax, or financial advice. Federal payment programs, IRS procedures, and benefit rules are subject to change. Readers should consult verified government sources or qualified professionals before making financial decisions or sharing personal information.