As January 2026 approaches, online interest in a possible federal $2,000 deposit has intensified. Search trends, video thumbnails, and social media discussions suggest that many Americans are expecting a significant government payment at the start of the year. For households managing rising costs, the idea of a $2,000 direct deposit is naturally compelling. However, understanding what this figure actually represents—and who may realistically see such an amount—is essential for avoiding confusion and financial missteps.

Unlike the pandemic-era stimulus checks that were authorised through emergency legislation, there is currently no universal federal program approving a flat $2,000 payment to all Americans in January 2026. Instead, the discussion reflects how the U.S. tax system operates each year, particularly during the early refund season. For many taxpayers, refunds generated through over-withholding and refundable credits often cluster around this amount, creating the impression of a special deposit when, in reality, it is the outcome of routine tax calculations.

Understanding the Origin of the $2,000 Figure

The $2,000 number has not appeared by accident. Over recent tax seasons, IRS data has consistently shown that the average federal tax refund falls close to this range. Refunds between $1,800 and $2,300 are common, especially among working families and individuals with dependents. Refundable credits, such as those linked to earned income or children, play a major role in shaping these totals.

Because January is when refund processing resumes, many taxpayers see deposits early in the year and naturally associate them with new government action. Headlines and social posts often simplify this pattern, framing typical refund outcomes as confirmed federal payments. Tax experts emphasize that a refund is not new income but a repayment of excess taxes paid throughout the year, combined with credits earned under existing law.

Who Is Most Likely to Receive a Deposit Near $2,000

Beneficiaries of January refunds are not a single group, but a broad segment of taxpayers. Lower- and middle-income households remain the most consistent recipients of refunds around $2,000. Families with children, single parents, and individuals working multiple jobs often qualify for refundable credits that increase refund amounts significantly.

Workers who experienced income changes in 2025 may also see higher refunds if tax withholding did not perfectly align with final earnings. Gig workers and contractors who made estimated payments may fall into this category as well. By contrast, higher-income earners are less likely to receive large refunds unless they deliberately overpaid during the year. Each return is assessed individually, making personal tax circumstances far more important than viral claims.

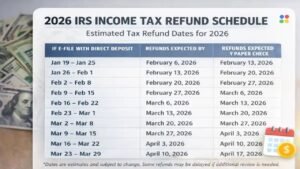

How the January 2026 Refund Timeline Typically Works

January marks the beginning of the refund cycle, not a single payout date. In the first part of the month, the IRS completes processing of amended returns and unresolved issues from the prior season. Once the new filing window opens, electronic returns with direct deposit are prioritized.

Taxpayers who file early, submit accurate information, and choose direct deposit often receive refunds within one to three weeks. Returns involving refundable credits may take longer due to mandatory verification checks, a process designed to reduce fraud. While some refunds arrive before the end of January, February remains the peak month for refund activity. This staggered schedule explains why experiences vary widely among filers.

Why Refunds Are Often Mistaken for Special Payments

The perception of a “federal deposit” is shaped as much by psychology as by policy. A refund arriving unexpectedly can feel like a bonus, even though it reflects taxes already paid. Round figures such as $2,000 reinforce the idea that the amount was intentionally chosen, rather than calculated through formulas.

Economic conditions amplify this effect. With inflation still influencing everyday expenses, many households feel more financial pressure than in previous years. As a result, refunds that once felt discretionary are now absorbed immediately by essentials such as housing, healthcare, and debt payments. This environment fuels the belief that additional assistance must be forthcoming.

Comparing January 2026 Refunds to Past Stimulus Checks

The contrast with pandemic-era stimulus programs is significant. Those payments were legislated, universal within income limits, and clearly communicated by federal agencies. The January 2026 refunds lack those characteristics. There is no new law, no single eligibility threshold beyond standard tax rules, and no official announcement of a fixed payment amount.

Similar misunderstandings have occurred in earlier decades whenever tax refunds coincided with economic uncertainty. In some years, smaller refunds triggered concern; in others, larger refunds sparked speculation about hidden benefits. The current situation reflects the latter, where ordinary refunds are interpreted as extraordinary relief.

What Beneficiaries Should Do Now

For taxpayers hoping to receive refunds early in 2026, preparation is more effective than anticipation. Ensuring that personal information is accurate, filing electronically, and selecting direct deposit remain the best ways to receive refunds quickly. Monitoring official IRS guidance is also critical, as misinformation spreads easily during tax season.

Financial planners encourage households to treat refunds as part of a broader financial strategy. Using funds to reduce high-interest debt, build emergency savings, or cover essential expenses often delivers more long-term stability than discretionary spending. Viewing refunds realistically helps prevent reliance on payments that may not materialize.

Looking Ahead: Could Federal Payments Change?

While there is no confirmed federal $2,000 deposit planned for January 2026, future policy changes are always possible. Discussions around tax credits and income thresholds continue, and any legislative action later in the year could influence future refunds. However, any such changes would be formally announced and implemented through established channels.

For now, clarity lies in understanding how the tax system already works. Refunds are calculated outcomes, not surprise announcements. For many Americans, a January deposit may indeed approach $2,000, but it will reflect individual tax circumstances rather than a new federal program.

A Balanced Perspective for 2026

The renewed attention around a $2,000 federal deposit highlights how closely financial security is tied to timing and perception. While hope for additional support is understandable, grounding expectations in verified information is essential. The most reliable path to financial stability remains careful planning, accurate filing, and informed decision-making.

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. There is no officially confirmed universal $2,000 federal deposit scheduled for January 2026. Refund amounts and timelines vary based on individual tax situations and IRS processing. Readers should consult official IRS resources or a qualified tax professional for personalized guidance.