As January 2026 approaches, searches for a “$2,000 direct deposit” have surged across the United States. From social media posts to online forums, Americans are eager to know if a new federal payment is on the way—and who might qualify. The interest is understandable: household budgets remain tight, inflation has eased but not disappeared, and memories of pandemic-era stimulus checks are still fresh for many families.

What makes this situation confusing is that deposits near $2,000 do appear regularly each January. Tax refunds, refundable credits, benefit adjustments, and delayed payments often arrive during this period, blurring the line between routine transactions and imagined stimulus programs. Understanding what is official—and what is speculation—is crucial to avoid financial missteps.

Why the $2,000 Direct Deposit Story Keeps Reappearing

The $2,000 figure carries historical significance. During the COVID-19 pandemic, Americans received multiple rounds of direct payments, including $2,000 checks proposed in political discussions. Since then, the number has become shorthand for “government relief,” even when no current policy exists. Each new tax season, screenshots of refunds or partial payments circulate online, breathing new life into old rumours.

Timing also contributes to confusion. January marks the start of large-scale IRS processing, and banks see a surge in deposits labelled as coming from the U.S. Treasury. Without proper context, these routine payments can be mistaken for a new programme. Media researcher Kavita Rao notes, “Repetition creates credibility. When people see the same number year after year, they stop asking where it came from.”

What Federal Agencies Have—and Haven’t—Announced

Despite widespread speculation, there is no official confirmation of a universal $2,000 direct deposit for all Americans in January 2026. The IRS, Treasury Department, and White House have issued no coordinated announcements, and no legislation authorising such a payment has passed Congress.

Former budget analyst Daniel Foster emphasizes why this matters: “A nationwide payment requires funding approval, administrative guidance, and weeks of public communication. None of those markers exist right now.” In short, the absence of official paperwork is a strong signal that viral claims are running ahead of reality.

Who May Still Receive Deposits Near $2,000

Even without a universal payment, many Americans will see deposits around $2,000 in early 2026. The most common source is the annual tax refund. Workers who overpaid through withholding or qualify for refundable credits such as the Earned Income Tax Credit (EITC) or Child Tax Credit can easily see refunds in this range.

Other legitimate deposits may come from amended tax returns, delayed benefit adjustments, or retroactive payments from Social Security or veterans’ programs. These payments are based on individual circumstances, not citizenship, which is often where confusion arises.

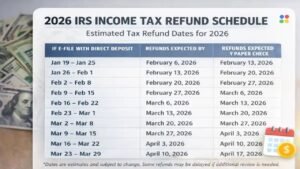

Why Payment Dates Differ Between Taxpayers

Another source of misunderstanding is the idea of a single payment date. Federal payments are released in batches rather than a single national payday. The IRS processes returns daily, and the Treasury distributes funds once returns clear verification checks. Banks then apply their own posting schedules, sometimes releasing funds immediately, sometimes holding them overnight.

This staggered system means two taxpayers filing on the same day may see deposits arrive days apart. Additional identity verification or credit reviews can stretch timelines further. As tax consultant Maria Jennings explains, “People expect precision, but the system is built for volume, not synchronisation.” The result is a rolling wave of deposits that can appear coordinated from the outside.

Scams and the Cost of Misinformation

Where confusion thrives, scammers often follow. Reports of emails and texts promising early access to a $2,000 January payment have already emerged. These messages frequently mimic IRS language, requesting bank details or processing fees. Federal agencies warn that legitimate payments do not require such actions.

The consequences go beyond stolen money. False expectations may prompt households to delay bills or make financial decisions based on income that will never arrive. Consumer advocate Helen Brooks stresses, “False hope is not harmless. Planning around imaginary deposits can create a bigger shock than having no hope at all.”

What to Expect in the Coming Months

Any genuine federal relief programme would be impossible to miss. Lawmakers would debate it publicly, agencies would update official websites, and mainstream media would provide clear guidance on eligibility and timelines. None of these steps have occurred. Current policy discussions remain focused on targeted credits and budget management rather than universal cash payments.

Economic relief may still appear in the future, depending on political and economic shifts. For now, experts recommend separating personal tax outcomes from national policy. Checking official IRS tools, reviewing deposit descriptions carefully, and ignoring viral countdowns remain the safest strategies.

Disclaimer: This article is published for informational and journalistic purposes only and does not constitute financial, tax, or legal advice. Federal payment amounts, eligibility criteria, and timelines depend on individual circumstances and government decisions. Readers should consult IRS publications, official agency websites, or qualified professionals for guidance specific to their situation.